KEY HIGHLIGHTS

- Philippine central bank signals no interest rate cuts for now as inflation rises

- Policy rate stays at 4.5%, easing cycle likely nearing the end

- Important watch for Singapore investors, FX traders, and regional banks

The Philippine central bank has made it clear: don’t expect interest rate cuts anytime soon. Inflation is creeping up again, growth has slowed, and policymakers are hitting pause after months of easing.

For Singapore-based investors, banks, and businesses with regional exposure, this decision affects FX movements, bond yields, loan pricing, and cross-border investments. No need to overthink — but definitely something to watch closely.

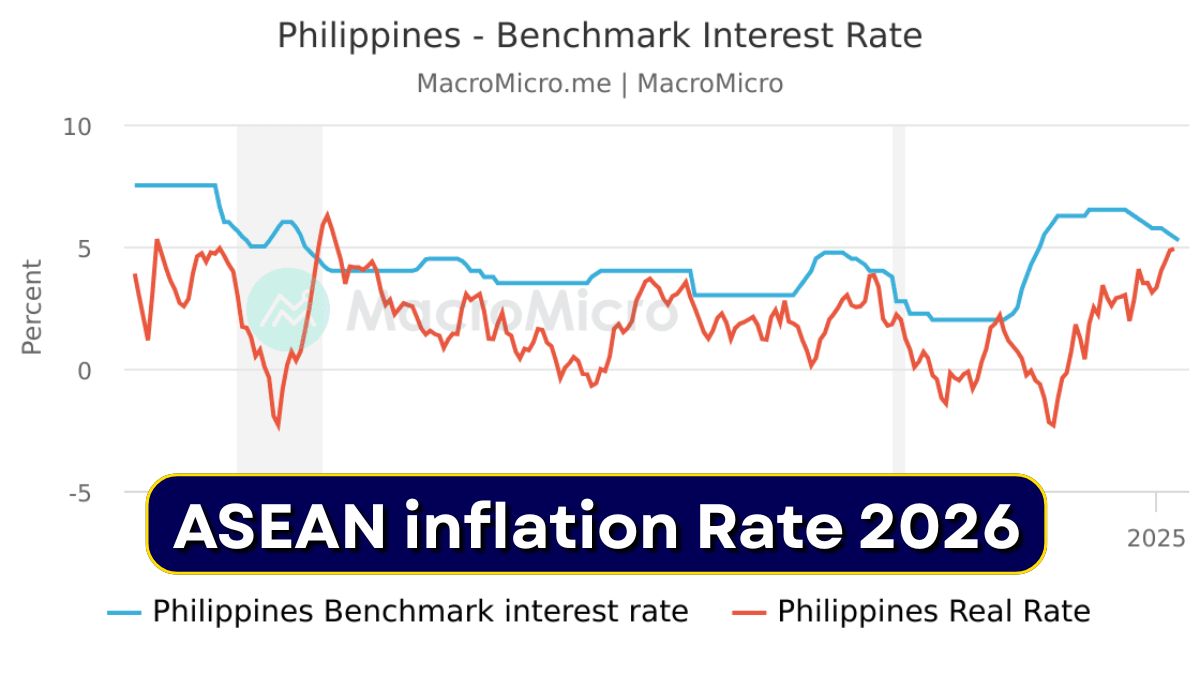

Inflation in the Philippines accelerated to 1.8% in December, the fastest pace in nine months, driven mainly by higher food and clothing prices. That’s up from 1.5% in November, according to official data.

| Key Indicator | Latest Figure | Why It Matters to Singapore |

|---|---|---|

| December inflation | 1.8% | Rising prices reduce odds of rate cuts |

| Monthly inflation jump | 0.9% | Sharpest rise since Sept 2023 |

| 2025 full-year inflation | 1.7% | Still low, but trend is turning |

| Policy interest rate | 4.5% | Impacts PH peso and SGD-PHP |

| 2025 growth estimate | 4.6% | Below government target |

What the Philippine Central Bank Actually Said

Governor Eli Remolona of the Bangko Sentral ng Pilipinas didn’t sugarcoat it.

Based on current data, rate cuts are off the table for now. The central bank believes it is already very close to its ideal policy rate, after cutting interest rates for five straight meetings last year.

The benchmark rate now sits at a three-year low of 4.5%, after a cumulative 200 basis points reduction since August 2024. Honestly speaking, this suggests the easing cycle is almost done.

There’s still a slim chance of another cut — but only if economic growth drops below 5%. Otherwise, expect rates to stay where they are.

Slower Growth Adds Pressure — But Not Enough (Yet)

Philippine economic growth in 2025 is estimated at 4.6%, down from 5.7% the year before and below the government’s earlier target of 5.5% to 6.5%.

The government has since trimmed its growth forecast to 5%–6% for this year and 5.5%–6.5% for 2027, citing global economic risks. Think higher-for-longer interest rates, weaker global demand, and regional volatility.

Still, the central bank expects growth to recover this year and next — which is why it’s choosing patience over rushing into more cuts.

Why This Matters for Singapore Investors and Businesses

For most Singaporeans, this isn’t just overseas news.

A stable or higher Philippine interest rate supports the Philippine peso, which affects SGD-PHP exchange rates, cross-border trade settlements, and regional investment returns.

If you’re invested in ASEAN equities, emerging market bonds, regional REITs, or fintech lending platforms, this policy stance influences capital flows and risk appetite.

Singapore banks and fund managers with exposure to the Philippines may also see loan demand slow while deposit yields remain competitive. For FX traders, volatility could pick up ahead of the next policy meeting.

What Happens Next: February Is the Key Date

The Philippine central bank’s next policy meeting is on February 19. That’s the next major checkpoint.

Officials have already signalled that any further easing will be limited and strictly data-driven. Translation? Inflation numbers and growth data will decide everything — not market pressure.

For now, the message is steady: rates stay put, unless conditions worsen sharply.

Frequently Asked Questions

Will Philippine interest rates be cut in 2025?

At this stage, it looks unlikely. The central bank has clearly said it is not planning further cuts for now, unless growth falls below 5% or inflation eases more than expected.

How does this affect Singapore investors?

It impacts currency movements, bond yields, and ASEAN investment flows. Singapore investors with Philippine exposure should expect stable yields but limited upside from rate cuts.

Should Singapore businesses be worried?

Not necessarily. Stable rates reduce uncertainty. However, slower Philippine growth could affect export demand, regional expansion plans, and loan growth.